A D V I S O R P R A C T I C E M A N A G E M E N T

BLOG

Why Investment only Financial Advisors and Portfolio Managers

must embrace Insurance and legacy Planning in 2026?

Why Investment-Only Advisors Must Embrace Insurance

Most investment-centric financial advisors begin their careers focused on portfolios—allocations, returns, and performance. It’s natural. The excitement of market dynamics, the constant news cycle, and the immediate feedback of gains and losses draw advisors and clients alike toward investments as the center of their conversations.

But here’s the reality: by staying locked into investments alone, many advisors unintentionally limit their value, their client relationships, and even the long-term profitability of their practices.

The truth is, your clients don’t just want better investment outcomes. They want peace of mind. And peace of mind doesn’t come from the market—it comes from knowing that, no matter what life throws at them, their financial plan can withstand the storms.

This is where life insurance, disability insurance, and critical illness coverage move from being “optional extras” to becoming essential pillars of your advice model.

Why advisors stay investment-focused

There are many reasons an advisor may not fully integrate insurance into their practice:

- Comfort zone: You were trained on investments, you’re good at them, and your process is built around them.

- Fear of pushback: Insurance is often misunderstood, and you may fear being seen as “selling” instead of “advising.”

- Complexity: The options, underwriting, and paperwork can seem like an unnecessary distraction from investment discussions.

Yet, staying investment-centric is like building only half a bridge for your clients. It looks impressive, but it won’t get them safely to the other side.

The potential you unlock

When you integrate insurance into your prospecting and client reviews, you do three things:

- Increase client value – You position yourself as the advisor who looks beyond returns and into the client’s whole financial life.

- Enhance the service experience – Clients feel safer, cared for, and more loyal when they know their risks are managed.

- Boost practice income – Insurance solutions provide a new, sustainable revenue stream that diversifies your business beyond investment fees.

In short, insurance makes your advice more complete, your practice more profitable, and your client relationships unshakable.

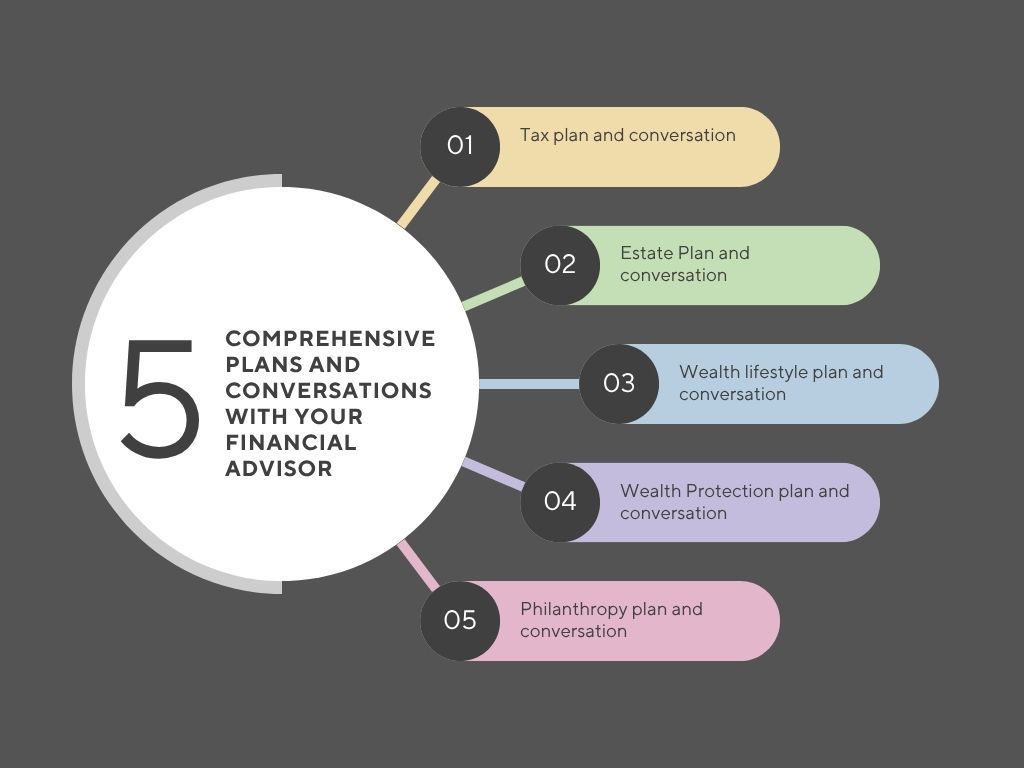

Life Insurance: The “Legacy Protector”

Why: Life insurance secures your client’s family, estate, and wealth transfer goals. It answers the question: “What happens to the people I love if I’m not here?”

How to Introduce It:

- In reviews, ask: “If something unexpected happened tomorrow, how would your family continue financially?”

- Use stories of families protected versus families unprotected—it brings the abstract into reality.

- Position life insurance as the foundation for wealth protection, not just another product.

Inspiring forward: Life insurance turns financial plans into legacies. Helping clients leave behind more than memories elevates your role from money manager to life architect.

Disability Insurance: The “Income Protector”

Why: Your client’s most valuable asset isn’t their portfolio—it’s their ability to earn an income. Disability insurance ensures that if health interrupts their career, their lifestyle doesn’t collapse.

How to introduce it:

- Ask: “If your income stopped tomorrow, how many months could you sustain your lifestyle before your savings ran out?”

- Frame disability coverage as a continuation of their investment plan: it funds contributions, lifestyle, and retirement goals even during a crisis.

Inspiring forward: Disability insurance keeps dreams alive, even when life blindsides your clients. You’re not just protecting dollars—you’re protecting decades of work, effort, and ambition.

Critical Illness Insurance: The “Recovery Cushion”

Why: Major illnesses don’t just impact health; they impact wealth. Treatment, time off work, and lifestyle adjustments can create financial stress exactly when focus and recovery should be the priority.

How to introduce it:

- Ask: “If you were diagnosed with cancer tomorrow, would you want the freedom to focus on recovery, or the burden of worrying about bills?”

- Present critical illness coverage as a “freedom fund”—cash that buys time, choice, and dignity in the face of adversity.

Inspiring forward: Critical illness coverage is about more than money—it’s about giving clients control when life feels out of control. You’re not selling insurance—you’re giving them options when they need them most.

How to put it all together

Here’s the framework to weave insurance naturally into your process:

- Start with empathy – Don’t lead with products; lead with understanding your clients' fears and aspirations. Show them that you care about their financial well-being and are committed to helping them achieve their goals.

- Link to goals – Position insurance as the safety net that keeps financial goals intact under any circumstance.

- Tell stories – People don’t remember numbers, but they remember stories of families protected and families left vulnerable.

- Integrate, don’t bolt-on – Insurance discussions should flow seamlessly into prospecting, planning, and reviews—not feel like an add-on.

The Bigger Picture: Practice Growth & Client Loyalty

Incorporating insurance elevates you from being a money manager to becoming a complete wealth advisor. It’s not just about better outcomes for your clients—it’s about:

- Stronger retention, because you’re delivering deeper value.

- More referrals, because you’re recognized for protecting not just assets but lives.

- Increased practice value, because diversified revenue streams make your business more resilient and attractive.

How to Implement

Do you need to be the insurance expert? Heck no! There are numerous insurance specialists all across the country willing to partner with you to become part of your in-house, outsourced team of experts to assist your clients in implementing their insurance needs. If you’re not familiar with this, let’s have a quick discussion!

Final word

Advisors who integrate life insurance, disability, and critical illness into their practice build something rare: a holistic, unshakable client relationship.

You’re no longer the advisor who manages investments—you become the advisor who protects dreams, futures, families, and legacies. That’s the kind of value that multiplies your impact, your income, and the ultimate worth of your practice.

The question is simple: are you ready to expand your conversations, elevate your role, and create the kind of practice that grows in both value and meaning?

Thank you for reading! This is what we help advisors do every day!

Would you like a copy of our Comprehensive Practice Management Checklist for financial advisors?

How About Your Goals for Your Practice in 2026?

While each financial advisor's practice may have a different approach, advisors need to understand where their practice needs help, and they will get the right help for the right part of their practice. What areas does your practice need help with?

Free Resources:

21 Page Technology Checklist to Become a Future-Ready Advisor

Fee Audit Checklist for Ideal Prospects

Updated Comprehensive PracticeManagement Guides

We are here to serve your practice. Let’s talk

Contact us to help get clarity around your goals on paper, and have the goals conversation by contacting Jeff at jeff@jeffthorsteinson.com or Grant Hicks, CIM at grant@ghicks.com

Regardless if we work together, let’s have a chat and listen to your biggest practice management concerns to help you get clarity around your future business.

To book a NO obligation conversation with me to discuss practice management or coaching, click the following link

Jeff https://calendly.com/jeffthorsteinson/30-minute-q-a-explore-apm

Grant https://my.timetrade.com/book/JMTNJ, Let’s have a conversation

Jeff Thorsteinson, Grant Hicks CIM and Advisor Practice Management's combined financial advisor clients manage over 8 billion AUM, and earn over $80 million dollars combined!